Each year the government sets a tax exemption limit or exclusion amount for estates under a. Phils estate does not need to use any of his 114 estate tax exemption when.

What Is Portability For Estate And Gift Tax Portability Of The Estate Tax Exemption The American College Of Trust And Estate Counsel

This is the amount a person can leave their heirs without paying federal estate taxes and which is annually indexed for inflation.

. Sue did not make a portability election. Phil passes away first when the federal estate tax exemption is 114 million. Two important aspects to remember are that the portability exemption is only available to married couples and only applies to Federal estate taxes.

Assume Phil and Dora are married and all of their assets are jointly titled. Understanding the portability of the estate tax exemption is crucial to ensuring your spouse has a clear understanding of how portability works. Why You May Want to Transfer Your Unused Estate Tax Exemption to Your Spouse December 17 2019 by Cathy Lorenz.

In this post we will discuss probably the most important estate tax election the estate tax portability exclusion. In 2022 you will be taxed if the total of the gross assets at hand exceeds 1206 million. The federal Estate Tax commonly referred to as the death tax is a tax on a persons right to transfer property upon their death.

The option of portability can make a significant difference when it comes to taxation of an estate. For individuals passing away in 2017 the estate tax is the tax applicable to any amount in the decedents estate over the Federal estate tax exemption of 549 million per person. Tax portability is a helpful tax benefit that should be considered when crafting your estate plan.

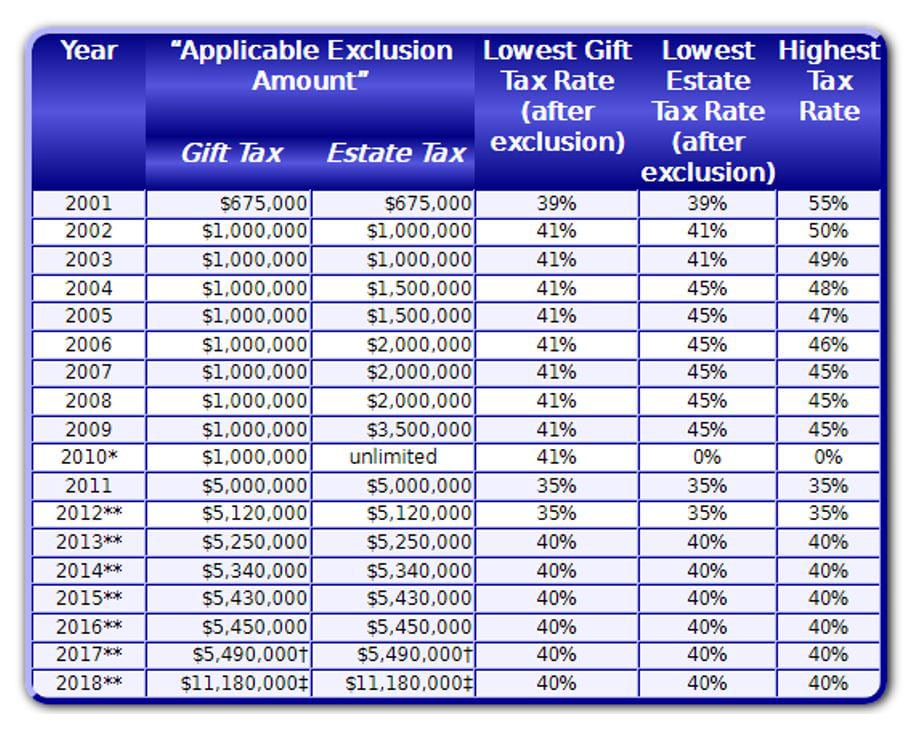

For 2019 the exemption sat at 114 million. Later in January of 2013 President Obama signed another important piece of legislation into law the American Taxpayer Relief Act ATRA. Why should we be concerned about estate tax if our estate is less than 1206 million.

The federal estate tax exemption and gift exemption is presently 1206 million. Why should we be concerned about estate tax if our estate is. Dont Throw Away a 1206M Estate Tax Exemption by Accident Many married couples fall into the portability trap They fail to file an.

Portability allows a surviving spouse the ability to transfer the deceased spouses unused exemption amount DSUEA for estate and gifts taxes to a surviving spouse so long as the Portability election is made on a timely filed federal estate tax return IRS Form 706. The portability feature means that when one spouse dies and his or her estate value does not use up to the total available estate tax exemption the unused portion of the estate tax exemption is then added to the available estate tax exemption for the surviving spouse. The federal estate tax exemption and gift exemption is presently 1206 million.

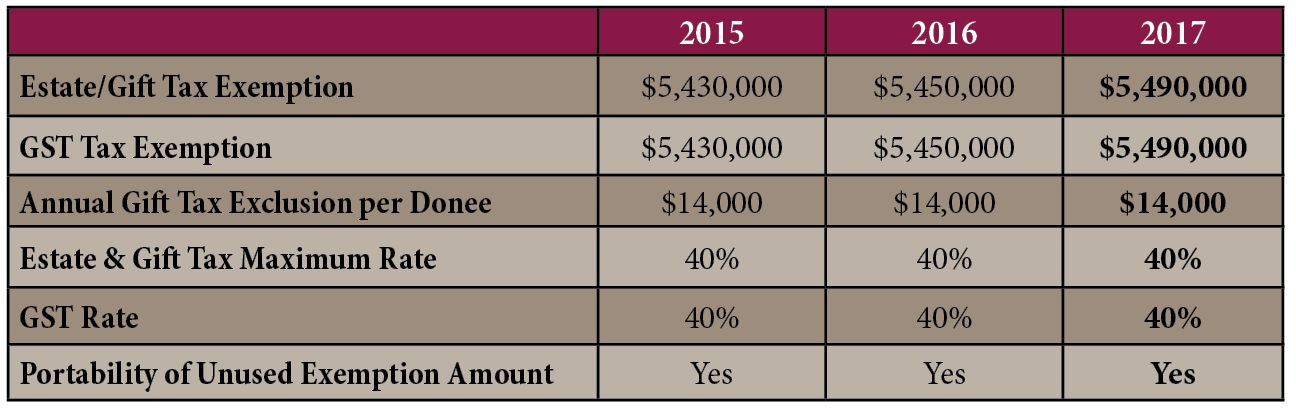

There are many options and exclusion when it comes to minimizing estate tax liabilities. Using the concept of portability of the estate tax exemption between spouses under these facts Franks unused 5340000 estate tax exemption will be added to Jennifers 5340000 exemption in turn giving Jennifer a 10500000 exemption. The exemption is tied to inflation so it will continue to rise.

Electing to use estate tax portability makes a significant difference in your federal estate tax liability. The portability of the federal estate tax exemption was introduced along with other significant changes to estate tax rules. In 2010 it increased to 1158 million.

Their net worth is 20 million. The ATRA made the portability of the estate tax permanent. When the surviving spouse passes away his or her estate will enjoy the.

Enter portability of the estate tax exemption. A married couple can transfer 2412 million to their children or loved ones free of tax with proper planning. Many married couples fall into the portability trap They fail to file an IRS form after one spouse dies and accidentally forfeit a massive federal estate tax exemption.

The Estate Tax With no Portability. If the estate representative did not file an estate tax return within nine months after the decedents date of death or within fifteen months of the decedents date of death if a six month extension of time for filing the estate tax return had been obtained the availability of an extension of time to elect portability of the DSUE amount depends on whether the estate has a filing. The estate tax is a tax on an individuals right to transfer property upon your death.

A married couple can transfer 2412 million to their children or loved ones free of tax with proper planning. Please note these laws being permanent means that they are not set. The exemption is tied to inflation so it will continue to rise.

Estate tax planning can be complex. Assuming that Sally has not used any of her estate tax exemption for lifetime gifts. Under portability if the first spouse to die does not use his or her exemption from estate and gift tax the executor of the first spouses estate may elect to give the use of the remaining exemption amount to the surviving spouse the so-called deceased.

Bidens Latest Estate Tax Exemption Proposal. The latest word from the Biden administration is that the estate tax exemption will be reduced effective January 1 2022 from the current 117 million per person enacted by the Trump administration in 2017 to the previous Federal limit of 5 million adjusted for inflation. There are only two states Hawaii and Maryland that have provisions for state estate tax portability as of 2020.

The Tax Relief Unemployment Insurance Reauthorization and Job Creations Act of 2010 introduced for the first time the concept of portability of the federal estate tax exclusion between spouses. Without portability if the first spouse died with an estate of 3000000 all of which passed to the Trust Exempt from Estate the deceased spouses unused estate tax exemption of 8400000 would be lost. The American Taxpayer Relief Act of 2012 ATRA made permanent the portability of estate tax exemption between spouses.

One is that many states have a state estate tax and in many of those states portability is not available for that state estate tax exemption. If the surviving spouse died with assets exceeding the federal estate tax exemption the surviving spouse could not use the lost exemption. Secondly it only applies to the federal estate tax exemption.

Each year the federal estate tax increases as it is indexed for inflation. So if youre in a state where this type of state estate tax would apply maybe there still needs to be some estate tax planning for both spouses. This is probably the 1 estate planning concept for married couples.

For example if Bob and Sally are married and Bob dies in 2011 and only uses 3000000 of his 5000000 federal estate tax exemption then Sally can elect to pick up Bobs unused 2000000 exemption and add it to her estate tax exemption.

The New Estate Tax Exemption And Portability Panacea Or Poison

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Estate Tax Introduction Video Taxes Khan Academy

Historical Estate Tax Exemption Amounts And Tax Rates 2022

A New Era In Death And Estate Taxes

Will Your Estate Be Taxable In The Future Context Ab

Tax Related Estate Planning Lee Kiefer Park

Historical Estate Tax Exemption Amounts And Tax Rates 2022

The 2017 Estate Tax Exemption The Ashmore Law Firm P C

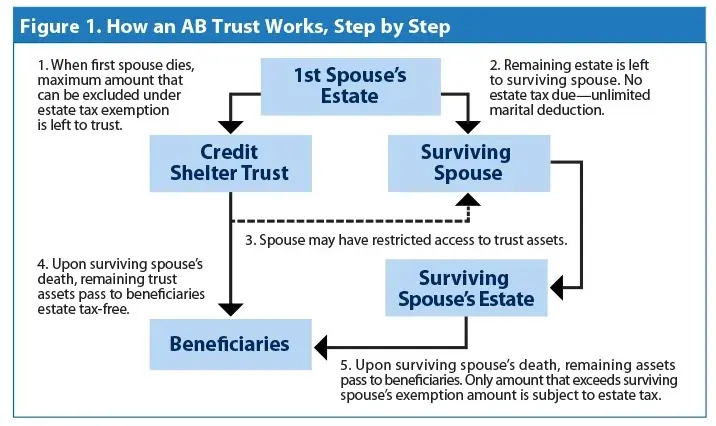

Is Ab Trust Planning Still Effective

What You Need To Know About The 11 Million Estate Tax Exemption Going Away

Estate Taxes Under Biden Administration May See Changes

Pin By Debbie Wolfe On Trusts Revocable Trust Living Trust Estate Tax

A B Trust Overview Purpose How It Works Advantages

Exploring The Estate Tax Part 2 Journal Of Accountancy

Wsj Tax Guide 2019 Estate And Gift Taxes Wsj

This Article Has Been Superceded New State Budget Increases The Connecticut Estate Tax Exemption Cipparone Zaccaro

This First Installment Of A Two Part Article On Everything Practitioners Should Know About The Estate Tax Includes The Unified Estate T Estate Tax Home Estates

Estate Tax Changes Under Recent Tax Acts Tyler Stone Group